Stop talking about 'greedflation'

Stop talking about 'greedflation'

It's mostly political PR-driven populism

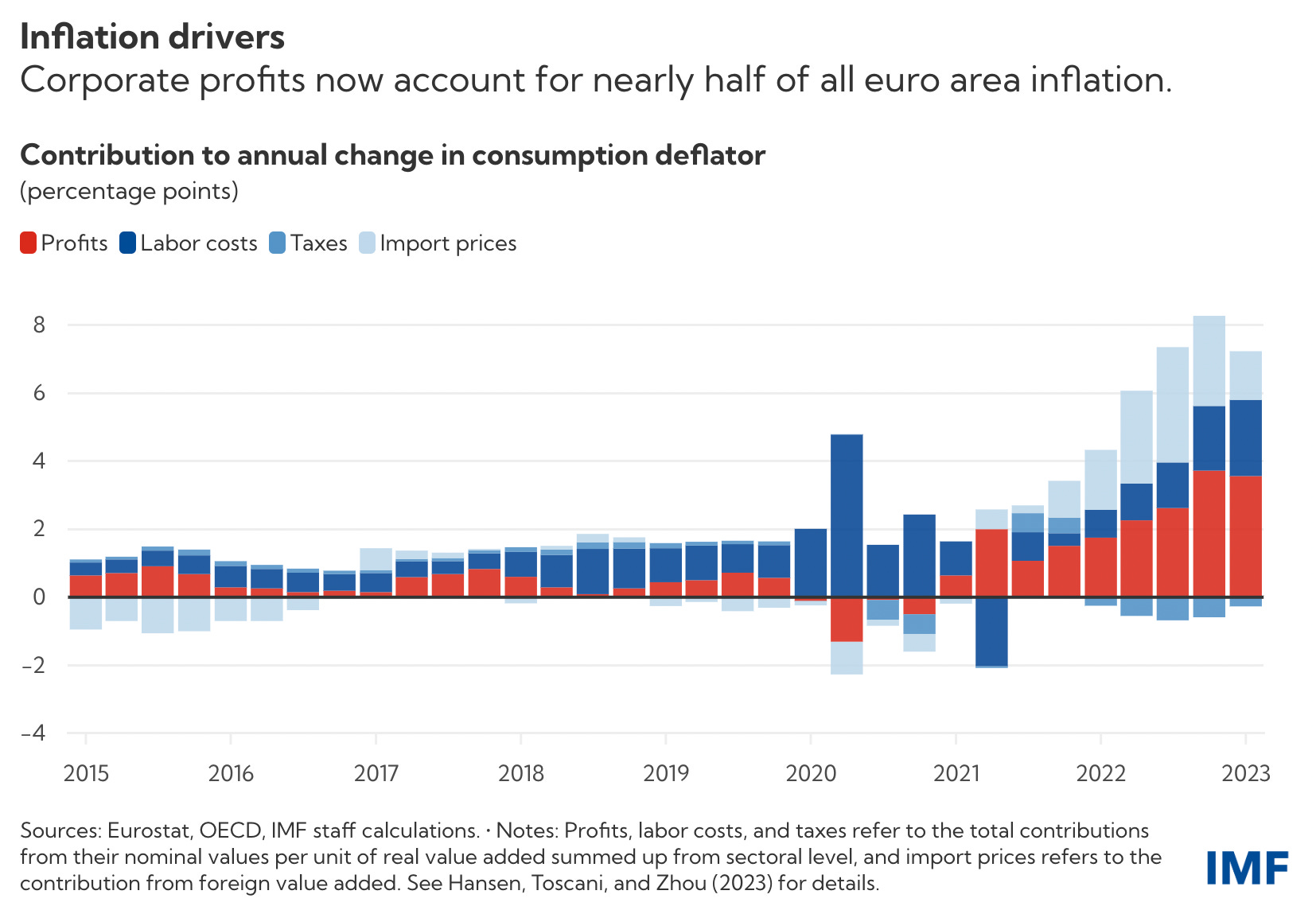

The International Monetary Fund has been publishing regular updates on the state of inflation in the eurozone, including data on what is accounting for inflation. After almost every update, populist commentators and politicians use these reports to blame private-sector profiteering for driving inflation. For them, the toll of Covid, years of borrowing and printing money, and the spending spree that came after are almost redundant in the face of corporate greed. They call it “greedflation” — a very misleading, mostly mythical term.

Commenting on the April report, Larry Elliot wrote in The Guardian that “companies have been able to use the crisis to drive up prices and boost profit margins”. After last month’s IMF update, MarketWatch used the term “greedflation” to describe what was going on in the graph above and declared that “IMF puts the blame for the rise in prices on corporate greed”.

Similarly, at peak inflation, when the US was going to the polls in November 2022 for midterm elections, Democrats blamed greedy firms for stirring inflation. Once Democratic presidential hopeful Senator Bernie Sanders claimed that “our economic crisis isn’t inflation, it’s corporate greed”.

Even though moderate Democrats, especially the one in the White House, weren’t fully endorsing this as a policy stance, the party’s communications strategists were advising candidates to shift the blame from the Biden Administration to ‘evil corporations’. Obama’s former communications chief, Dan Pfeiffer, said that “Democrats have a winning message on inflation if they use it: focus on corporate greed, which is driving up inflation”.

Weirdly enough, while Turkey was battling much higher inflation at the same time, the Erdogan Government was blaming secular CEOs for not helping tackle the issue and the police were raiding companies holding onto big stocks of food. (Surprise: Inflation is still high in Turkey!)

Clearly, this is good messaging for governments. However, the problem is just that: it’s only messaging. Greedflation is not an economic truth and corporations didn’t cause inflation. Their profits increased because of the economic factors that triggered inflation since they had to hike prices in the face of increased demand and spending.

What the IMF does is accounting, calculating what accounts for inflation, not establishing a causal link between corporate profits and inflation — because there isn’t one.

Greed doesn’t explain inflation

The main issue with blaming greed is that it doesn’t explain inflation. If greed is the problem, why isn’t there unending inflation since private markets are driving our economies all the time? Do they only get greedy from time to time? Are they too lazy at other times? Of course not. Corporations are always greedy but inflation is not always a problem.

Inflation is, by definition, an exogenous phenomenon. Temporary shocks to the economy set it off and move prices away from their market values. Optimal prices are set on market factors like demand, supply, costs, expectations and risks. It’s not a coincidence that the overwhelming majority of corporations hate inflationary periods. Inflation increases risks and costs, requires the re-adjusting of prices, and leads consumers to change behaviour. The increase in prices, which drives the temporary rise in profits, comes from the increase in risk factors and financial expectations. It doesn’t come from thin air.

One reasonable argument would be that during inflationary periods, consumers’ price perceptions get shattered thus giving the companies an opportunity to hike prices unfairly. This could explain the persistence of inflation but cannot explain why inflation rose in the first place.

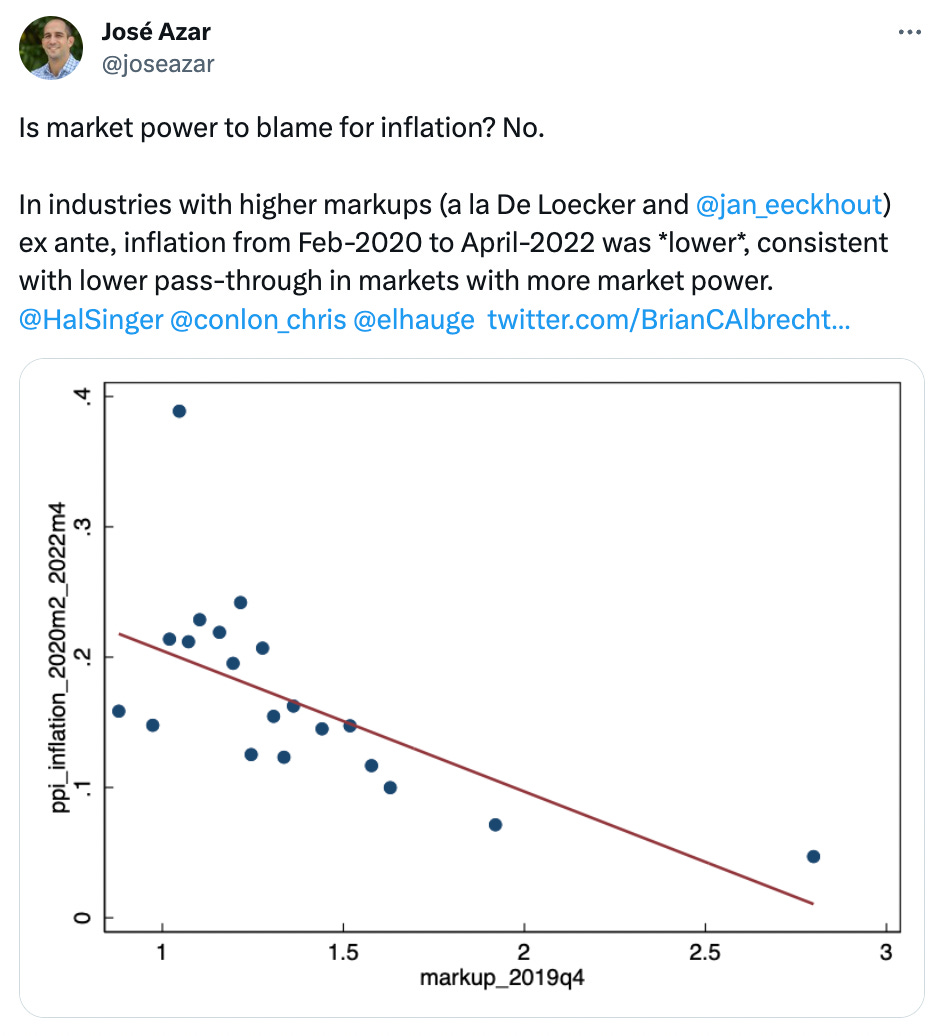

Even if a firm decided to increase prices unreasonably during an inflationary period, its competitors wouldn’t follow which would make them more attractive to the clients they both try to reach. Only monopolies have this power but they have it all the time — not only during periods of inflation. Why are they using it only now?

The US (and much of the world) was battling high inflation in the 1970s, when market concentration was at historic lows. Markets have been getting less and less competitive since then but inflation stayed low consistently for decades, which shows that monopolies by themselves cannot be responsible for inflation either.

Accordingly, the Biden White House’s annual economic report for 2023 highlighted monopolistic companies’ possible anti-competitive behaviour in theory but also cautioned that greed and monopolies cannot be the only reason behind inflation:

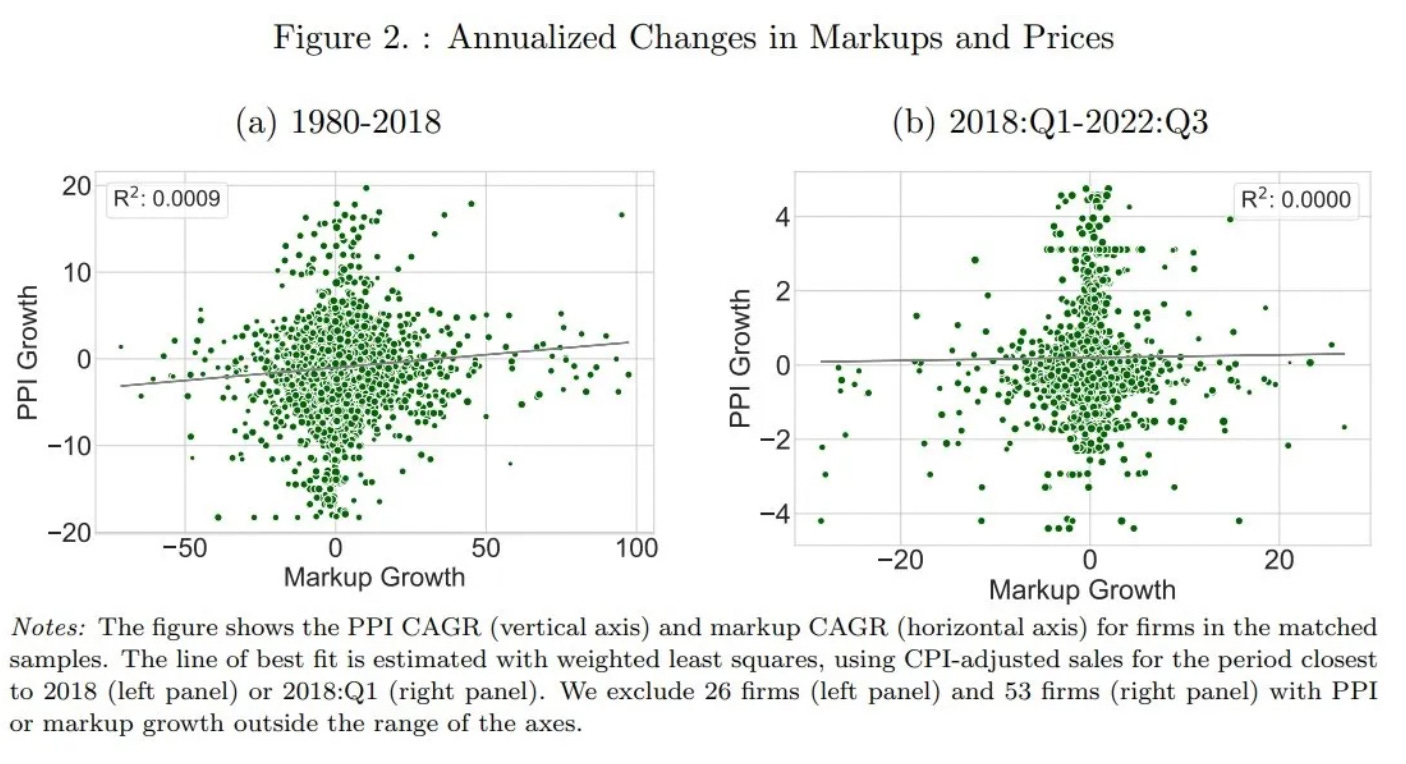

The link between market power and pricing when subject to shocks like the pandemic is not clear. . . . Measuring market power is a difficult task, and measuring the prices firms charge above the cost of their inputs, their ‘markup,’ isolated from the effects of the increased demand and constrained supply of 2022, is even more fraught.

Actually, excluding energy, which had extraordinary fluctuations for non-economic reasons, in markets with clear dominant firm(s) the effects of inflation was felt less than more competitive markets. The price hiking came mostly from the weaker players in the economy, probably because they had less capacity to increase supply when demand soared.

So, what actually happened?

Well, we spent a lot of money.

The rise in profit margins in the US started before the inflationary attack and it was due to the injection of money into the economy during the Covid lockdowns, which also arguably triggered inflation. The fiscal stimulus accounted for 25% of the GDP and included three rounds of cheques sent to the citizens.

When people have money to spend, it’s likely that they will spend it. That’s what they did.

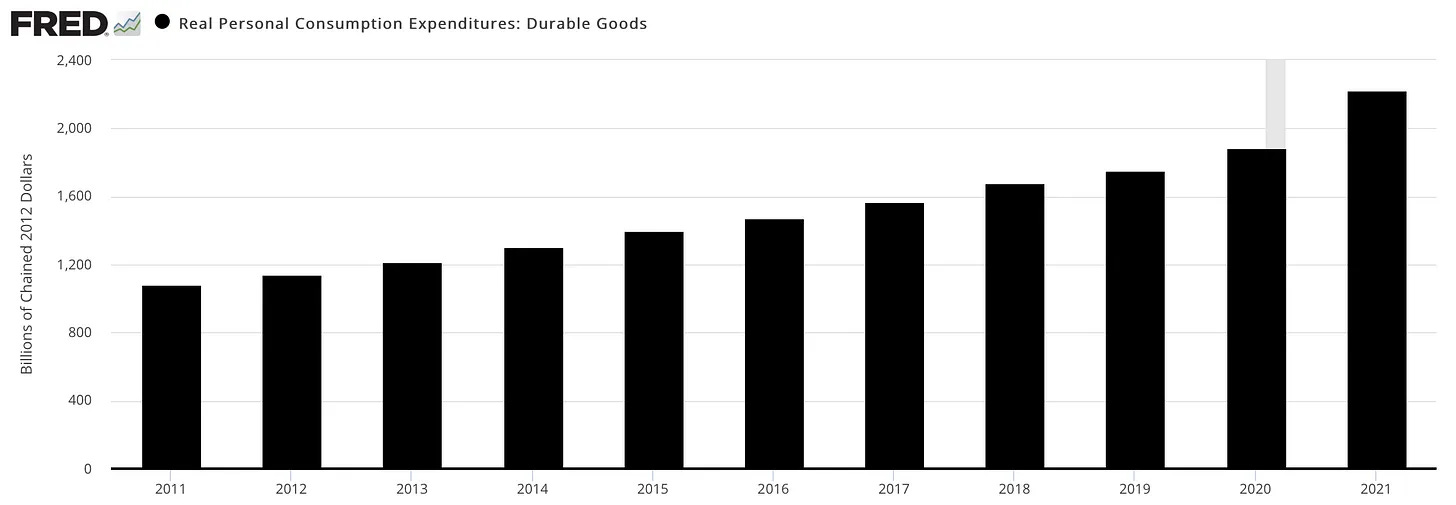

As seen below, people bought more durable goods than ever before:

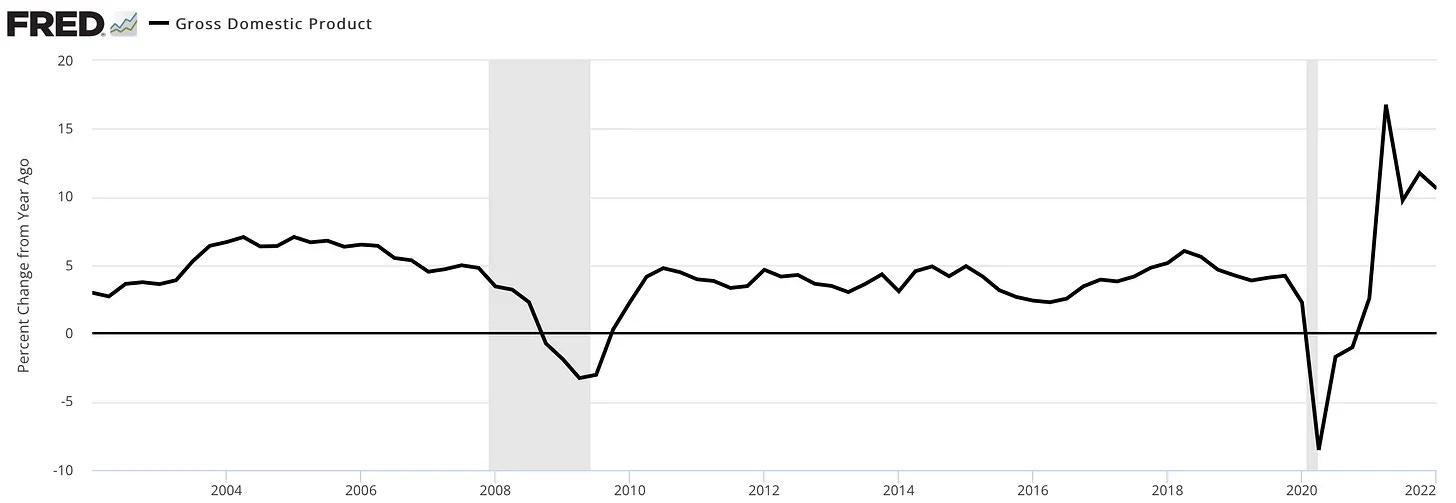

This was reflected in the US’s spending growth as well. The short period of economic pause of lockdowns were followed by a historic catch up:

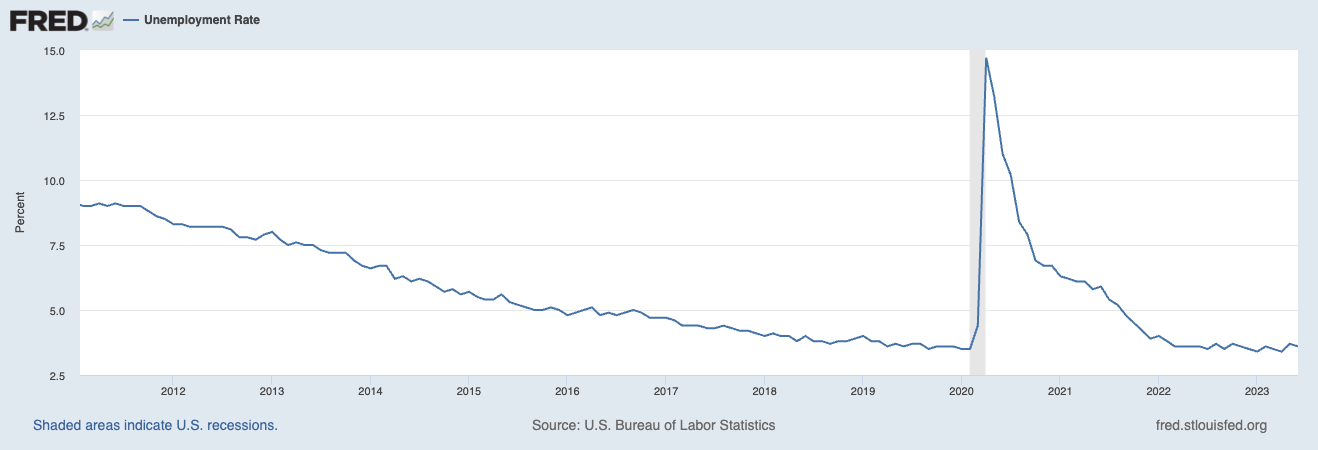

Which was followed up by new people joining the workforce to match production with spending:

When people start buying stuff faster than they are being produced, prices go up. This is not being evil and greedy, it’s how business works.

Let’s assume you are producing t-shirts. You were used to getting 100 orders a week, which almost came to a halt at the start of the pandemic. However, shortly thereafter, you started getting 130 orders a week because the government put some money in your potential customers pockets (rightly) but you lack the staff and materials to catch up with the orders. Let’s say that you hired new people but you know that this is a temporary state of business, reminded by a Russian dictator causing instability in energy prices — you’ll not invest in more production capabilities because the market may return to normal before they pay for themselves. What do you do? You increase prices and make 130 orders of profit by producing 120 t-shirts.

In a macroeconomic level, this looks like high demand and spending (new orders), low unemployment (the new hires) and increased profits (the new pricing policy). Remember supply chain crisis? It was more of a demand crisis. This is what happened and even though corporate profits were high during inflationary times, they have been falling even as consumer prices continued to rise.

The main reason behind this is that the risk factors decreased and economic expectations are much more positive now. Companies that increased prices with worse expectations have been pushing the breaks. Accordingly, a study in Belgium showed that “price increases in 2022 were mainly driven by higher input prices, suggesting that initial import price shocks gradually spread to all sectors”. Similarly, the Federal Reserve of Kansas City concludes that fear was a better explanation for price hikes than greed:

The decline in markups during the first half of 2022—even as inflation remained high—is consistent with firms having raised markups during 2021 in anticipation of future cost pressures. Furthermore, the growth in markups was similar across industries with very different relative demand and inflation rates in 2021, which is also consistent with an aggregate increase in expected future marginal costs. We conclude that an increase in markups likely provides a signal that price setters expect persistent increases in their future costs of production.

Greedflation is the lag between price and wage hikes

What looks like greed is mostly an accounting lag.

Simply put, prices are easier to increase than wages, which are subject to more rigidities like being set by previous wage negotiations. However, as profitability rises for companies, wages follow. Unsurprisingly, labour costs picked up over recent quarters, as highlighted by the IMF (above) and US data.

Here’s the IMF itself emphasising that blaming companies for causing inflation would be unrealistic:

[There must be] caution against an over-simplistic interpretation where an increase in gross operating surplus is interpreted as corporate profits being the largest driver of inflation.

Overall, greed doesn’t cause inflation but corporate profits may increase during inflationary times. The factors that actually cause inflation are the same as the factors that increase profits: Injecting more money into the economy gives rise to demand which increases prices. Additionally, inflation also messes up financial and economic expectations, forcing firms to decrease risks by further price hikes. Blaming companies for this process may be politically useful but it’s economically unrealistic.

Thankfully, policymakers didn’t take the greedflation myth seriously till now. If they start doing so, they’ll only create new problems. You can’t heal a broken leg with Vitamin C.

Interesting stuff…

This blog post, Innovation Is Slowing Down, by Adrian H. Raudaschl is great. We have been talking a lot about innovation in the past decades but we aren’t as innovative as before. This has many reasons — we already innovated a lot and new things are increasingly niche, state spending on R&D has been falling etc — and the article is a great summary of many. Here’s a great bit: In the early days of the Prize, scientists were an average of 37 years old when they made their prizewinning discovery. But in recent times, the average age has risen to 47, an increase of approximately a quarter of a scientist’s working career.

Former US Secretary of State, Condoleezza Rice, argues in an article published in 2000 that the invention of the internet, advances in personal computing and more generally the technological leap at the end of the 80s are essential to understand why the US became the ‘winner’ of the Cold War. Innovations that create new markets, rather than disrupting existing ones, are the drivers of economic growth — which explains Rice’s thinking.

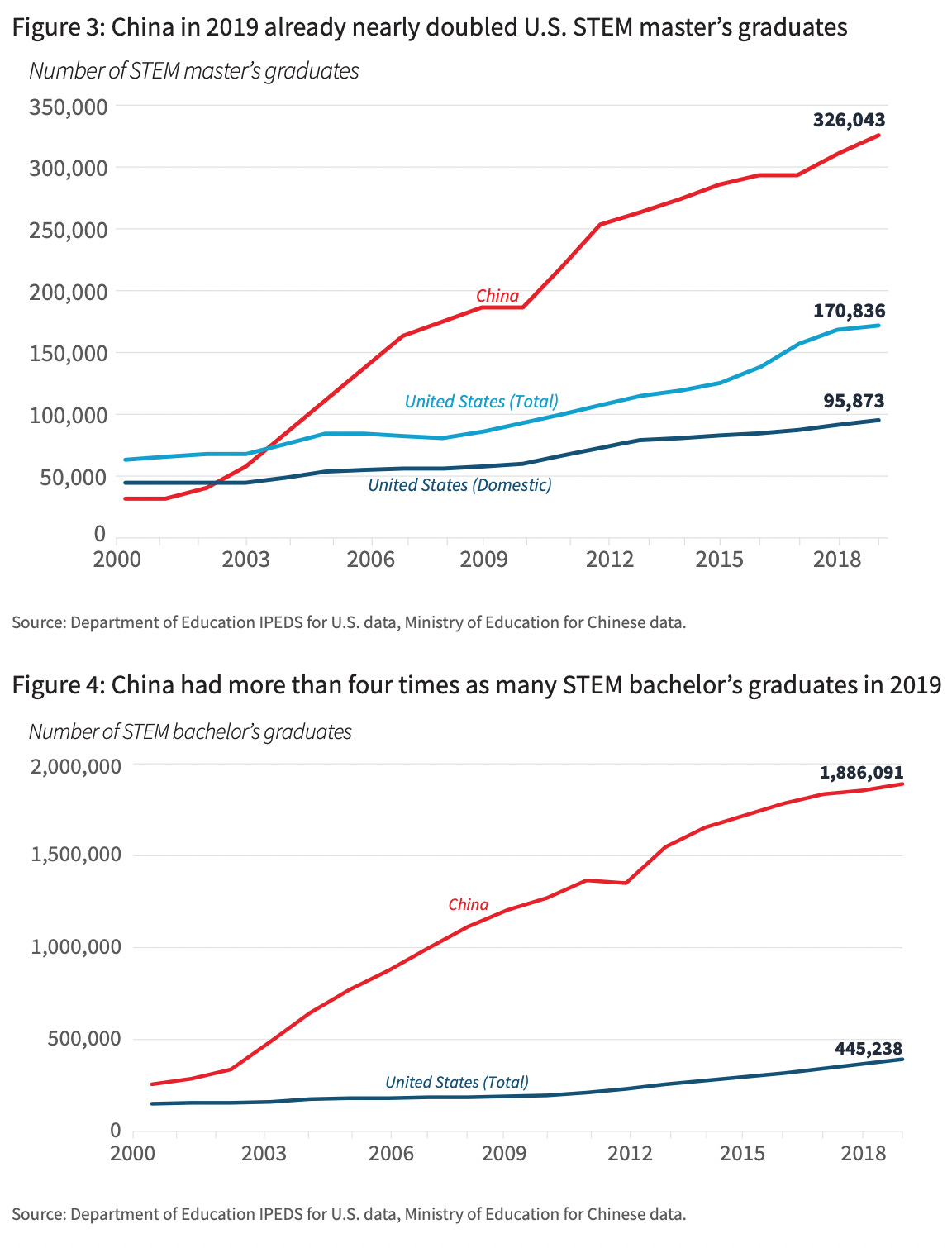

Related to the first point, this CSIS report, Winning the Tech Talent Competition, is extremely important in understanding our age’s great power rivalry. The race between the US and China will have a great technological component and the US’s most effective weapon on this front is its ability to attract talent. Knowing that China will never be as attractive as the US, the Chinese Government has been investing in domestic reforms and education, promoting STEM degrees. Even though are now way ahead of the US in granting bachelor’s and master’s degrees (lagging behind on PhDs), they are getting only a fraction of talented immigrants. That’s one of the reasons why I love working on migration policy. Singapore’s founding leader (and probably the most competent politician of the past century), Lee Kuan Yew spoke to Joseph Nye, a leading International Relations scholar from Harvard in 2015 on this great power rivalry. Here’s a great quote:

I asked Lee Kuan Yew whether he thought China would overtake the United States as the leading power of the 21st century. He said “no,” because the United States is able to re-create itself by attracting the best and brightest from the rest of the world and melding them into a diverse culture of creativity. China has 1.3 billion people to recruit from domestically, but in his view, its Sino-centric culture makes it less creative than the United States, which can draw upon a talent pool of more than 7 billion people. That is, as long as we remember that we are indeed a nation of immigrants.

… and a book!

Lee Kuan Yew’s memoir is the best political autobiography I have ever read. When he ‘founded’ Singapore, it was a small unproductive land with a deeply divided and poor society. When he left the helm of the country, it was one of the richest and most productive. Yew’s personal story is the amazing success story of Singapore. The title is fitting: From Third World to First. (Buy the book via this Amazon link and Jeff Bezos will pay some of his profits to me!)

There are incredible details in it. My favourite is this: One of the first few things Yew accomplished as Prime Minister was to build a great road from the airport to the PM’s residence. This was planned as a special ride for potential investors and government officials, showing what Yew’s ideal Singapore would look like. They built high-rise apartments and office blocks for the few talented workers they had, green spaces and the productive machinery of government on that road.

Many invested.

You’ll find amazing insights on management, business, economics, bureaucracy, politics and international affairs in it.

Can’t recommend it enough.